Who is eligible for Medicare in Massachusetts?

Table of Contents

To be eligible for Medicare Part A or Part B, you must be a U.S. citizen or a legal permanent resident who has lived in the United States for at least five consecutive years in the state of Massachusetts. You must be 65 years old or older in most cases. If you are disabled, you may qualify for Medicare prior to age 65.

If you're new to Medicare and unsure where to start, here's a quick breakdown of what makes you eligible for coverage in Massachusetts.

Medicare Eligibility Requirements in Massachusetts

You are generally eligible for Original Medicare Parts A and B if you are a U.S citizen or have been a legal permanent resident for at least five continuous years. If you meet one of these criteria, you will be eligible for Medicare in Massachusetts:

- You are 65 years old or older

- You are under 65 and permanently disabled

- Have End-stage renal disease (ESRD)

- Have Lou Gehrig's Disease, also known as ALS (Amyotrophic Lateral Sclerosis)

The disability path runs on its own clock. "If you're receiving Social Security Disability (SSDI), you automatically get Medicare after 24 months of benefits. You'll receive your Medicare card automatically," says James Hale, a licensed Medicare agent in Georgia. He notes two important exceptions: "ALS: Medicare starts the same month as SSDI. End-Stage Renal Disease (ESRD): Earlier eligibility possible." If either condition applies, Massachusetts residents don't have to wait out the standard two-year window. For ESRD specifically, Medicare typically starts the third month after regular dialysis begins. Coverage can begin sooner for Massachusetts residents who enroll in a home dialysis training program or receive a kidney transplant.

For a broader look at the program itself, see our guide on what Medicare is and how it works.

A person who has been receiving monthly Social Security benefits or Railroad Retirement Board (RRB) benefits for at least four months before turning 65 does not have to file separate applications to be eligible to premium-free Part A. The individual in Massachusetts will automatically receive Part A at 65 in this instance.

How to Apply for Medicare in Massachusetts

Individuals who are not receiving RRB or Social Security benefits monthly must apply for Medicare. Contact the Social Security Administration to file an application.

Part A coverage starts the month an individual turns 65. If you sign up after your Initial Enrollment Period and qualify for premium-free Part A, coverage can be backdated up to 6 months (but never earlier than the month you turned 65). Waiting longer than that means losing out on those retroactive months.

An individual who turns 65 on the first of each month will have Part A coverage. This applies to the person whose 65th birthday falls on the first of the following months. If an individual's 65th birthday falls on December 1, Part A coverage begins on November 1.

In Massachusetts, Am I Automatically Eligible for Medicare When I Turn 65?

Yes, unless you actively decline Medicare Part B coverage because you’re still working and receiving employer-based healthcare benefits. When you turn 65, most people are eligible for Original Medicare (Parts A and B). If you’re already collecting Social Security, the paperwork takes care of itself. "If you are already retired AND collecting Social Security, congratulations! A few months ahead of your birth month you will be AUTOMATICALLY enrolled in Medicare A and B," says Charles Wheeler, a licensed Medicare agent in Massachusetts. "You will be sent a card in the mail showing your Medicare ID# and effective dates. If you plan on using Medicare as your health insurance moving forward you do not need to take any further action."

If you’re still working and have employer-based health insurance, you can defer Medicare until you stop working and come off of your employer’s health insurance plan. Your employer can't push Massachusetts workers off their plan just because they hit 65, either. "Your employer can not force you to take Medicare when you turn 65," says Tamela Clayton, a licensed Medicare agent in Texas. "You can delay enrollment into Medicare as long as you have other creditable coverage. If you do not enroll when you are first eligible — and you do not have other creditable coverage — you may be subject to a late enrollment penalty if and when you do decide to enroll. That late enrollment penalty will be attached to your monthly premium for as long as you have Medicare." For details on how this works, see our guide on Medicare and employer coverage when working at 65.

Who Is Not Eligible for Medicare in MA?

Individuals who don't meet the above requirements will not be considered for Medicare coverage. Here's how it breaks down:

To qualify for premium-free Part A (meaning you pay no monthly premium for hospital insurance coverage), you need enough work credits — officially called Quarters of Coverage (QCs). You earn these credits by working and paying payroll taxes under the Federal Insurance Contributions Act (FICA). Most workers pay full FICA taxes throughout their career.

"If you have accumulated 40 quarters of qualified work, your Part A is a $0 premium benefit," says Mark Bilgere, a licensed Medicare agent in Texas. "It is not free, as you have been contributing during your working life. If you do not have 40 quarters or your spouse doesn't have 40 quarters (you qualify if your spouse has them), then you can purchase Part A for the current year cost."

For age-based Medicare, you can qualify based on your own work history or a spouse's work record. Credits from a parent or child only come into play for certain disability-based eligibility situations. The number of credits required depends on whether you're applying based on age (typically 40 credits, or about 10 years of work), disability, or End-Stage Renal Disease.

If you haven't earned enough credits, you can still enroll in Part A, but you'll pay a monthly premium. Medicare Savings Programs may help cover these costs for eligible Massachusetts residents with limited income. Those who qualify for both Medicare and Medicaid may be eligible for additional assistance through dual eligibility.

Individuals in Massachusetts who are eligible for premium-free Part A can enroll at any time, even if they are not automatically enrolled.

What Does Medicare Cost Once You're Eligible?

Once you qualify for Medicare, it's important to understand what you'll actually pay. Most people pay no premium for Part A because they (or a spouse) earned enough work credits. However, Part B carries a standard monthly premium that CMS updates each year, and higher earners may pay more due to IRMAA surcharges. You can check the current standard Part B premium and deductible on the official Medicare.gov costs page before you enroll.

Beyond premiums, you'll also be responsible for deductibles, copayments, and coinsurance under Original Medicare coverage. Many Massachusetts residents choose to add a Medicare Supplement (Medigap) plan or a Medicare Advantage plan to help cover these out-of-pocket costs. You may also want Medicare Part D prescription drug coverage to help pay for medications.

Free, Local Medicare Help in Massachusetts

Massachusetts residents can get free, unbiased Medicare counseling through the State Health Insurance Assistance Program (SHIP). SHIP counselors are trained volunteers who can walk you through eligibility, enrollment, plan comparisons, and billing questions — without trying to sell you anything. Every state has a SHIP, and services are free. You can find your local Massachusetts SHIP office through shiphelp.org or by calling 1-877-839-2675.

Medicare Enrollment Windows in Massachusetts

Individuals who wish to enroll in premium Part A, B, or both must enroll during the enrollment periods set out by law, which apply in Massachusetts. These enrollment periods are applicable to premium Part A as well as Part B.

- Initial Enrollment Period

- General Enrollment Period

- Special enrollment Periods

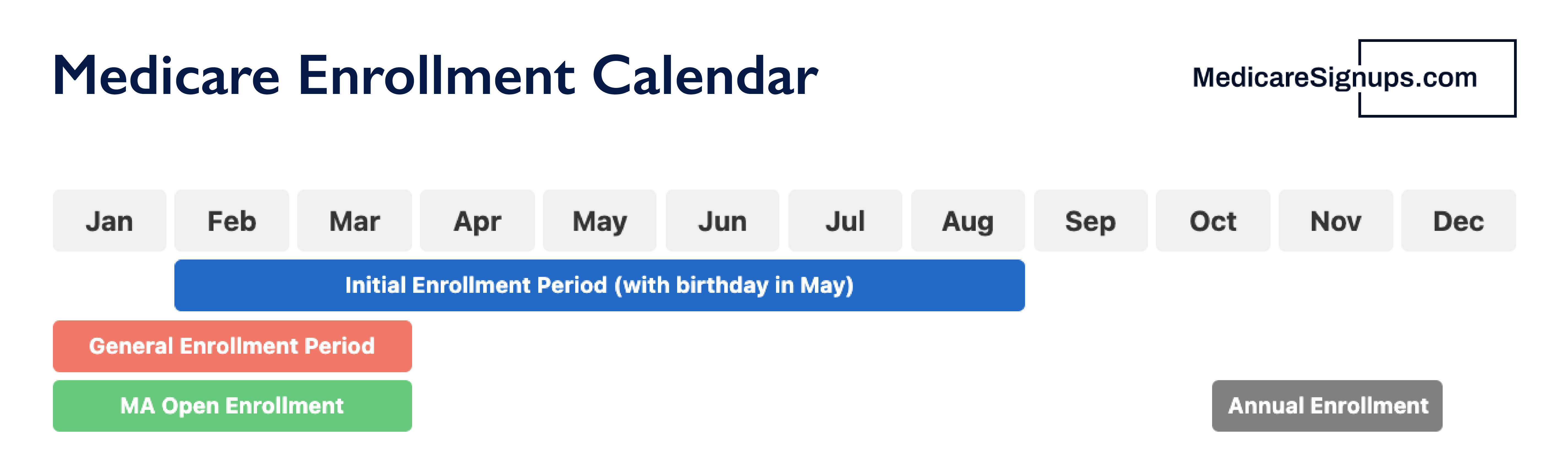

Massachusetts Initial Enrollment Period (IEP)

The IEP is a period of 7 months that starts 3 months before a person turns 65. It ends 3 months later. If you qualify for Medicare because of a disability, your IEP is tied to your 25th month of receiving Social Security Disability (SSDI) benefits. It starts three months before that 25th month, includes the 25th month itself, and ends three months after. Individuals with ESRD or ALS have a different IEP. It depends on the individual's situation.

The month following a person's IEP enrollment, coverage will start. After receiving disability benefits from Social Security, a disabled person is automatically enrolled in Medicare Part A or Part B.

Most people will be charged a late enrollment penalty if they do not enroll in Part A or Part B when they are first eligible. For as long as you hold Part B, you'll be charged the Part B penalty. The one way around the penalty is having what Medicare calls creditable coverage. "Creditable coverage means you already have health or drug coverage that Medicare considers good enough to delay signing up without getting penalized later," says Jason Denniston, a licensed Medicare agent in Indiana. "This matters because Medicare late enrollment penalties can stick with you for life, especially for Part B and Part D. The tricky part is that employer coverage, VA benefits, COBRA, and retiree plans all follow different rules, so it's important to know what counts before you delay enrollment." Understanding common mistakes first-time enrollees make can help Massachusetts residents avoid these costly penalties.

Massachusetts General Enrollment Period (GEP)

GEP is a three-month period that runs from January 1 to March 31 each year. If you enroll during the GEP, your Part A and Part B coverage will begin the following month.

Massachusetts Special Enrollment Periods (SEP)

You can sign up for Part A (or Premium Part A) in certain circumstances without having to pay a late enrollment penalty. The Special Enrollment Period is available only for a short time. If the person does not sign up during the Special Enrollment Period they will have to wait until the next General Enrollment period and may have to pay a monthly late enrollment penalty.

The month following a person's enrollment during their SEP, coverage will start.

SEP for the Working Aged or Working Disabled in MA

Individuals in Massachusetts who are not eligible for Part B or premium part A because they were covered by a group plan based on their current employment or that of a spouse (or that of a family member if disabled) can enroll during this SEP.

An individual can sign up at any time during current employment or the 8-month period beginning with the month that ends in which the group's coverage ends.

This SEP is not available to individuals with ESRD.

Katelyn Malotte

Licensed Massachusetts Medicare Agent

Contact Katelyn through Medicare Agents Hub »

Matt Feret

Author, Prepare for Medicare - The Insider’s Guide

https://prepareformedicare.com

Matt Feret is the author of the Prepare for Social Security - The Insider’s Guide and the Prepare for Medicare - The Insider’s Guide book series and launched PrepareforSocialSecurity.com to help people get objective answers to questions about Social Security and Medicare. Matt is also the host of The Matt Feret Show. He has held leadership roles at numerous Fortune 500 Medicare health insurers in sales, marketing, operations, product development, and strategy for over two decades.